Ruida Futures: Both ends of supply and demand improve Shanghai zinc shock

Client

Abstract: After the Brexit referendum, the market's safe-haven demand will cool down, and the basic metal market will return to the fundamentals again. The zinc market fundamentals have strong improvement expectations this year. At the supply end, the global zinc mine shortage expectation, coupled with the structural reform of the domestic supply side, is expected to reduce the supply pressure of refined zinc. On the demand side, China's steady growth demand is strong, while supply-side reforms will not abandon demand-side stimulus, which will help boost demand in the zinc market.

First, the fundamental analysis

(1) The monetary environment of major economies in the world is loose

Whether the global monetary easing environment can be maintained is the most important focus of the current macro aspect. In Japan, the yen continues to appreciate, exports are damaged, and the economy is weak, so the policy of monetary easing will continue. In Europe, the economic outlook is not good; the Fed’s delay in raising interest rates has led to a small space for the euro to depreciate; in addition, in response to the risk of the UK’s “Brexitâ€, ECB officials generally believe that easing is still very useful. In the US, the US economic data is mixed. The spillover effect from the downward pressure on the global economic growth has caused the Fed to be cautious in advancing the rate hike. The market is not optimistic about the interest rate hike, and the real interest rate remains. At the negative interest rate level. In China, due to the large fluctuations in the stock market in the second and third quarters of last year, more liquidity was injected to maintain market stability, which led to a significant increase in the M2 base at that time. In the case of normal growth of M2 in the next few months, its year-on-year growth rate may still have a significant decline. However, this does not mean that the domestic monetary environment has a tendency to tighten. The main tone of future monetary policy operations to maintain steady growth and support the development of the real economy will not change.

(2) New environmental protection law and supply-side structural reforms to increase production contraction

The new environmental protection law, which was implemented on January 1, 2015, has a long-term effect on changing the status quo of the extensive development of the basic metals industry. The increase of environmental protection has made the industrial chain from zinc mining to refined zinc smelting tend to intensive development. In recent years, small mining and smelting enterprises will gradually withdraw from the market, and the expansion of supply side will be greatly slowed down. In addition, the supply-side structural reforms that have once again become hot spots will have a more significant impact on zinc supply. De-capacity and compression of inefficient supply will further limit the increase in zinc production. At the same time, we should pay attention to the supporting infrastructure and high-end manufacturing financial support in the supply-side reform process, which cannot be ignored. In addition, we need to pay attention to the process of resource tax reform. On May 10, the Ministry of Finance and the Ministry of Finance issued the "Notice on Comprehensively Promoting the Reform of Resource Taxes", which will start in July 1st, 2016, in gold mines, copper mines, bauxite mines, lead-zinc mines, nickel mines, In the 21 resource areas, such as tin mines, the implementation of the mineral resource tax ad valorem reform. After the resource tax reform, the profitability and risk assessment of short-term non-ferrous mining companies may improve, but the profit elasticity of long-term non-ferrous mining companies has decreased. The implementation of the principle of ad valorem increase after the resource tax reform means that in the upward cycle of mineral prices, the tax pressure of non-ferrous mining enterprises will increase with the upward price, so the profit elasticity of enterprises has declined. This also means that if the zinc price rises sharply, the enthusiasm for the company to increase production is suppressed, and the business activities can reflect a more stable feature.

In the past two years, a series of domestic policies have been favorable for maintaining the stable operation of non-ferrous metals prices, and the policy warm wind will play a role in supporting zinc prices.

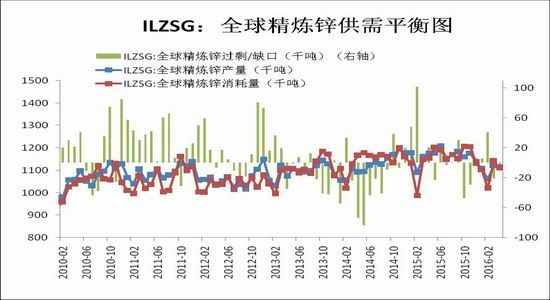

(3) Global supply and demand balance

According to data released by the International Lead and Zinc Research Group (ILZSG), the global zinc market has a surplus of 24,000 tons in the first four months of this year, which is much narrower than the surplus of 185,000 tons in the same period of last year. The data indicates the global zinc supply and demand fundamentals year-to-date. There has been a significant improvement. However, the global zinc supply gap narrowed to 2,500 tons in April, and the shortfall was 20,400 tons in March. The main reason is the rebound in China's output. China's zinc mine output (zinc content) increased by 5% to 456,000 tons in April. The rise in zinc prices boosted China's output. The advancement of China's supply-side structural reforms and the expectation of a global zinc mine shortage have determined that there will be some resistance to the increase in zinc output in the future. It is expected that the fundamentals of the zinc market will continue to improve, and the zinc price will be formed in the medium and long term. Another agency, the World Bureau of Metal Statistics (WBMS) released a monthly report saying that in the first four months of 2016, the global zinc market had a surplus of 6,700 tons, which was a significant improvement over the 2015 annual surplus of 106,000 tons. Among them, global refined zinc production in the first four months decreased by 4.5% year-on-year, and demand rose by 0.4% year-on-year. According to WBMS data, China's zinc demand increased by 5.6% year-on-year in January-April, and domestic refined zinc production fell by 0.7% year-on-year. According to the World Bureau of Metal Statistics, the fundamentals of the domestic zinc market have improved significantly compared with last year, which is basically consistent with the conclusions of the ILZSG report published in the same period.

figure 1

Source: Ruida Futures, data source: ILZSG

(4) Domestic refined zinc supply

According to the latest statistics from the Bureau of Statistics, the national refined zinc output in May 2016 was 533,000 tons, an increase of 5.75% from the previous month and an increase of 2.1% from the same period of last year. From the accumulated data, the cumulative production in January-May was 2.485 million tons, an increase of 0.5% year-on-year. There was a continuous small increase in the month-on-month, indicating that the domestic zinc smelting production gradually recovered after the Spring Festival; the year-on-year data showed that the output in May rebounded moderately in comparison with previous years. According to a survey conducted by Shanghai Nonferrous Metals (SMM), the operating rate of domestic key zinc smelting enterprises in May was 74.8%, an increase of 0.95% from April. However, according to the size of the company, the average operating rate of large enterprises (with an annual production capacity of more than 200,000 tons) fell by 0.96% to 81.98%. In June, although some of the early maintenance companies resumed production, Shaanxi Zinc Industry, Hanzhong Zinc Industry, and Chifeng Zhongxin added new inspections, which affected production. The remaining manufacturers had no obvious increase in production plans. SMM expects the operating rate of smelters in June to fall slightly to 73.61% from May. On the whole, this year's demand is difficult to be significantly stimulated, and with the advancement of supply-side reforms, coupled with the expected impact of tight global zinc supply, the supply side is expected to maintain a moderate recovery.

figure 2

Source: Ruida Futures, data source: National Bureau of Statistics

From the aspect of import and export, domestic refined zinc continues to maintain a steady increase in exports and shrinking imports. According to customs data, China's refined zinc exports from January to May were 8,697 tons, down 85.4% year-on-year; during the same period, 259,252 tons of refined zinc were imported, up 45.9% year-on-year; cumulative net imports were 250,000 tons, up 112% year-on-year (132,567 tons). The import of refined zinc accounted for one-third of the domestic supply, which made the supply of domestic refined zinc market abundant, and there was no shortage of supply. The increase in the supply of refined zinc is partly converted into inventories. We observe the situation of Shanghai zinc stocks in January-May. According to the exchange data, the apparent inventory of refined zinc by the end of May was 230,557 tons, an increase of 15% from the end of last year, which is 30,100 tons. However, from the beginning of April to the end of June (end of June), the domestic refined zinc inventories showed a continuous decline, which occurred in the context of increased supply. This may indicate that the balance of supply and demand in the first half of the year is undergoing subtle changes, and the increase in demand is stronger than the increase in supply. However, whether this part of the demand is the actual consumption of the real economy or the transfer to invisible stock for other purposes, we need to further explore below.

image 3

Source: Ruida Futures, data source: General Administration of Customs

Figure 4

Source: Wind, data source: previous issue, LME

(5) Primary consumption areas

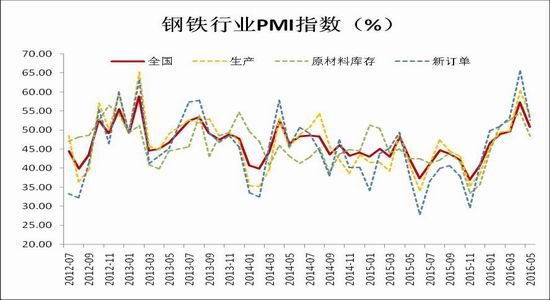

Galvanized steel and galvanized steel are the most important primary consumption areas for refined zinc. The situation in the steel industry indirectly reflects the demand for refined zinc. According to the statistics of China Federation of Iron and Steel Logistics Professional Committee, the PMI index of the steel industry in May was 50.9%, down 6.4 percentage points from the previous month. It fell again after five consecutive months of recovery, but it has been at 50 for two consecutive months. % above the line of glory. Among the main sub-indices, the production index and the new order index both fell, but they still maintained the expansion range of more than 50%. The decline of the new order index was significantly larger than the decline of the production index, indicating that the market demand fell more obviously, and the supply exceeded the demand pressure. The new export order index continued to rise, and it was in the expansion range of more than 50% for two consecutive months. The export orders of iron and steel enterprises remained at a high level; the finished goods inventory index rebounded sharply, and returned to more than 50% after 9 months. The expansion range shows that the steel company contract organization is not smooth, and there is a backlog in inventory. PMI shows that the current production and operation activities of iron and steel enterprises are still in a state of expansion, and production and demand are maintained at a relatively high level. However, there are signs of oversupply in the industry, and there is a backlog in enterprise stocks. The short-term weakness of the domestic steel market is still difficult to change.

Figure 5

Source: Ruida Futures, data source: Wind database

Let's take a look at zinc oxide, galvanizing, die-cast zinc alloy and so on. According to a survey conducted by Shanghai Nonferrous Metals (SMM), the operating rate of zinc oxide enterprises continued to rise to 62.3% in May 2016. The company's research targets 30 zinc oxide enterprises, involving a production capacity of 428,200 tons, mainly concentrated in Jiangsu, Shandong, Hebei, Shanghai, Liaoning and other places. The tire industry's operating rate continued to be high in April-May, and the support for zinc oxide orders was relatively obvious. It entered a slight contraction in June. According to the scheduling plan, the operating rate of zinc oxide enterprises is expected to decline slightly to 58-59% in June. The zinc oxide market is in a tepid state, indicating that there is still no significant recovery in demand in the zinc market. According to the Shanghai Nonferrous Metals (SMM) survey, the operating rate of galvanizing enterprises in May was 89.04%, a decrease of 7.04% from the previous month. In terms of scale, the operating rate of large enterprises in May (annual production capacity of 100,000 tons or more) was 88.98%, down by 7.2% from the previous month, and the operating rate of small and medium-sized enterprises fell by 4.8% to 90.2%. The operating rate of galvanized manufacturers declined in May, mainly due to environmental pressure, seasonal demand and low price fluctuations. It is expected that the operating rate of enterprises will remain at around 88% in June, with a limited decline, but the operating rate will continue to decline in July, putting pressure on zinc demand. According to a survey conducted by Shanghai Nonferrous Metals (SMM), the operating rate of die-cast zinc alloy enterprises in May was 65.6%, down 3.2 percentage points from the previous month. In June, on the one hand, the pressure on environmental protection of enterprises has increased, and the enthusiasm for starting work has been suppressed. On the one hand, the rapid rise in prices has led to an increase in fears of their end customers and a reduction in the amount of inventory that affects purchases; on the other hand, locks, automobiles, zippers, etc. The off-season demand has dragged down related parts orders. Therefore, the operating rate of enterprises will continue to decline. It is expected that the operating rate of die-cast zinc alloy will be 62.5% in June, down 3.05% from May. From the above aspects, we can get such a conclusion. The effect of the off-season consumption in the second quarter is obvious. The primary consumer market in the zinc market is still relatively weak, and there has not been a clear improvement. However, such a weaker consumption is more likely to be attributed to seasonal factors, and further expectations need to be analyzed from the direction of the end consumer market.

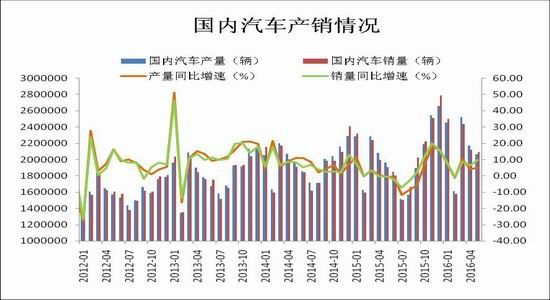

(6) Terminal consumption field

According to the latest statistics released by China Association of Automobile Manufacturers, in the first five months of this year, China's automobile production and sales were 10.84 million and 10.755 million, respectively, up 5.8% and 7% over the same period of the previous year, up from 2.6 and 4.9 in the same period of last year. Percentage points. However, after entering the low season of consumption, the monthly data showed a decline. In May, the production and sales of automobiles were 2.065 million and 2.092 million respectively, down 5.1% and 1.7% respectively from the previous month, and up 5% and 9.8% respectively. On the whole, the development of China's auto market is still relatively healthy. In the future, after the off-season consumption, production and sales are expected to rebound as expected. By then, it is expected to boost demand in the zinc market.

Figure 6

Source: Ruida Futures, data source: National Bureau of Statistics

This year, China's real estate industry is surging, or a new situation has emerged. First- and second-line housing prices have risen in turn, and the inventory pressure on the third- and fourth-line real estate markets has increased. In the trade-off between preventing asset bubbles and stabilizing growth, the government is facing an unprecedented dilemma. However, the current outcome is that the real estate market is still growing. According to the statistics of the Bureau of Statistics, the total area of ​​new housing starts in the first five months of this year reached 5,952,600 square meters, an increase of 18.3% year-on-year, reversing the downward trend of last year. In the same period, the cumulative investment completed was 356.41 billion, an increase of 7% year-on-year, and remained at a relatively high level. It is expected that the real estate market will remain a market that the government has to maintain in the second half of the year. It has far-reaching implications for economic stability, but there may be new means for structural regulation. But no matter what, demand for the zinc market is expected to be more profitable than bad.

Figure 7

Source: Ruida Futures, data source: National Bureau of Statistics

Second, the conclusion

After the Brexit referendum, the market's safe-haven demand will cool down, and the basic metal market will return to the fundamentals again. The zinc market fundamentals have strong improvement expectations this year. At the supply end, the global zinc mine shortage expectation, coupled with the structural reform of the domestic supply side, is expected to reduce the supply pressure of refined zinc. On the demand side, China's steady growth demand is strong, while supply-side reforms will not abandon demand-side stimulus, which will help boost demand in the zinc market. From a macro perspective, the Brexit provides more reasons for the Fed to continue to postpone the rate hike, which has weakened the negative impact of the Fed’s interest rate hike. On the face of the disk, the main contract of Shanghai Zinc continues to rebound in the shock, and the medium and long-term line can be optimistic. It is suggested that the Shanghai Zinc 1609 contract will be slightly adjusted to 15600 yuan/ton for multiple orders, the target for the second half will be 17,500 yuan/ton, and the stop loss will be 14,900 yuan/ton.

Third, the operational strategy

1. Risk preference advice

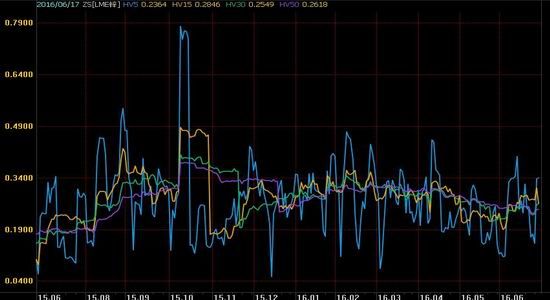

Due to the high correlation between the LME market and the domestic Shanghai zinc market, historical volatility we chose LME zinc for analysis. Short-term volatility rebounded within a month, mainly due to mood swings caused by the Brexit referendum. As of June 28, the 5-cycle volatility was 0.3361, a high of nearly two months. The medium-term volatility also showed a certain degree of recovery, with a 15-cycle volatility of 0.3116 and a 30-cycle volatility of 0.263. However, the long-term volatility continued to fall, with a 50-cycle volatility of 0.2482, which was a low in the year and has continued to decline since March. The increase in volatility caused by short-term single-risk events is expected to be unsustainable. In the long run, the volatility is still narrowing, and the volatility characteristics are suitable for conservative traders.

Figure 8

Source: Wind, Data Source: LME

2. Long-term investment in the second half of the year

After the Brexit referendum, the market's safe-haven demand will cool down, and the basic metal market will return to the fundamentals again. The zinc market fundamentals have strong improvement expectations this year. At the supply end, the global zinc mine shortage expectation, coupled with the structural reform of the domestic supply side, is expected to reduce the supply pressure of refined zinc. On the demand side, China's steady growth demand is strong, while supply-side reforms will not abandon demand-side stimulus, which will help boost demand in the zinc market. From a macro perspective, the Brexit provides more reasons for the Fed to continue to postpone the rate hike, which has weakened the negative impact of the Fed’s interest rate hike. On the face of the disk, the main contract of Shanghai Zinc continues to rebound in the shock, and the medium and long-term line can be optimistic. It is suggested that the Shanghai Zinc 1609 contract will be slightly adjusted to 15600 yuan/ton for multiple orders, the target for the second half will be 17,500 yuan/ton, and the stop loss will be 14,900 yuan/ton.

3, arbitrage (cross-month arbitrage, cross-species)

(1) Cross-month arbitrage: Shanghai-zinc monthly contracts are far higher and lower, and since the monthly contract price difference is maintained at 50 yuan/ton, the arbitrage opportunities are small, and there is basically no profit space. Cross-month arbitrage is not recommended for operation.

(2) Cross-species arbitrage: The two metals of lead and zinc have a tendency to be consistent due to the existence of symbiosis and common features, but their fluctuations are not the same. Since the beginning of the year, the price difference between zinc and lead has been rising, mainly due to the difference between the two fundamentals. This year's improvement in zinc fundamentals is expected to be strong. There is no bright spot in addition to the round of supply factors before and after the Spring Festival. The fundamentals are high, and the zinc-lead price gap has risen sharply. As of June 29, the price difference between Shanghai and Shanghai reached 3,275 yuan / ton, a record high in the past year. It is expected to continue to climb in the future. Operationally, the strategy of multi-zinc lead is carried out near the spread of 2500-2700 yuan/ton.

Figure 9

Source: Futures, Data Source: Previous Period

4, the hedger (demand, seller)

Demand: Shanghai zinc has been improving for a long time, and demanders have increased their inventory. At the same time, they can consider implementing a buy-in hedging strategy. Operationally, the Shanghai-Zinc main contract will buy a 40% position at 15,600 yuan/ton; if the market continues to go down, it will build a 40% position at 15,200 yuan/ton; the remaining 20% ​​will depend on the market.

Vendor: In view of the long-term expectation of zinc price, the short-term hedging position of the seller can be appropriately reduced in the second half of the year (30%-50% is appropriate), and the spot is appropriately increased. If the Shanghai zinc main contract rebounds to 17,000 yuan / ton, the short position will be controlled below 50%, and the rebound to 17600 yuan / ton will consider increasing the short position to 80%. The hedge position is appropriately operated according to the market fluctuations.

Ruida Futures Research Institute

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Our LED Emergency Batten Light is perfect for commercial and industrial use, made from solid polycarbonate with a thick poly carbonate diffuser the unit is very durable this fitting has an IP rating of 65 and is anti corrosive. Interal lithium battery pack to make emergency time rating from 60-180mins. The fitting gives off an impressive 5850 lumens using only 65 watts of energy making it a great energy saving light fitting. The batten uses high quality LED chips giving off a great array of light to any indoor and outdoor area.

Emergency Batten Light,Emergency Led Batten,Emergency Light Batten,Led Emergency Batten Light

Foshan Nai An Lighting Electric Co.,ltd , https://www.articalight.com